Key Takeaways:

- Vans remains a work in progress: Vans’ revenue declined 5% in constant currency in Q4 and posted an 11% full-year decline, but Americas DTC returned to growth for the first time in almost four years.

- The North Face delivered standout Q4 performance, with global revenue up 7% in constant currency and Americas up 16%, capping a year in which the brand grew more than 5%.

- VF Corporation returned to full-year revenue growth for the first time in three years, with executives pointing to margin expansion, debt reduction, and brand momentum as evidence the turnaround is real.

VF Corporation reported fourth-quarter and full-year fiscal 2026 results that executives say signal an inflection point for the Denver-based apparel and footwear conglomerate, even as one of its most important brands, Vans, continues to lag the rest of the portfolio.

Total VF Q4 revenue rose 3% in constant currency to $2.2 billion (excluding Dickies), with The North Face and Timberland both posting gains and the Altra running brand surging 45%.

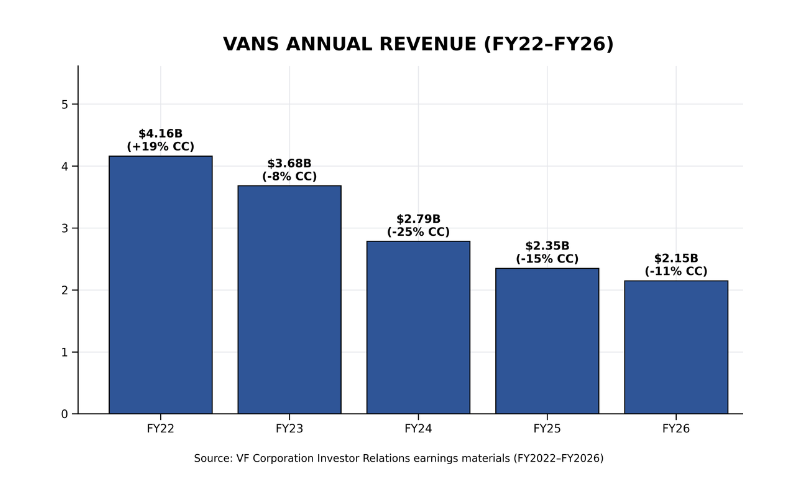

Vans, meanwhile, declined 5% in constant currency for the quarter and posted an 11% full-year revenue decline, though the brand showed early signs of stabilization in the Americas. For fiscal year 2027, Vans’ revenue is expected to decline again.

“Americas is more than 50% of (Vans’) total business, and it’s where the trends start for Vans,” VF CEO Bracken Darrell said on the call. “If you remember, our (Vans) e-com business in the Americas first turned to growth in Q3 of 2026 with 4% growth. In Q4, Americas total DTC grew 5%. The Americas is the foundation for the brand’s energy. This is where we said the recovery would start, and as the Americas DTC continues to grow, its brand heat will start to show up elsewhere.”

Companywide, Darrell said VF’s Q4 and full-year results are a confirmation that VF’s multi-year transformation is taking hold.

“For the first time in three years, we returned to a full year of growth and expect to keep growing in fiscal 2027,” Darrell said in a statement. “We also significantly expanded margins and reduced our leverage ratio by a full turn versus last year. In the fourth quarter, we delivered our strongest revenue performance since I joined VF.”

VF Corp. Q4 and Full-Year Fiscal 2026 Financial Results

All figures are in constant currency unless otherwise noted and exclude Dickies, which the company sold in late 2025.

VF Q4 Fiscal 2026

- Total revenue: Up 3% to $2.2 billion compared to Q4 fiscal 2025.

- The North Face revenue: Up 7% in Q4; Americas up 16%.

- Vans revenue: Down 5% in Q4; Americas up 3% driven by DTC.

- Timberland revenue: Up 2% in Q4.

- Altra revenue: Up 45% in Q4.

- Adjusted earnings per share: $0.00 vs. a loss of $0.14 in Q4 fiscal 2025.

- Americas: Up 10% in Q4, the region’s highest growth rate since Q1 fiscal 2023.

- EMEA: Down 5%.

- APAC: Up 1%.

- Direct-to-consumer revenue: Up 2%.

- Wholesale revenue: Up 3%.

VF Full-Year Fiscal 2026

- Total revenue: Up 1% in constant currency, excluding Dickies, compared to fiscal 2025.

- Adjusted gross margin, excluding Dickies: 55.2%, up 110 basis points vs. fiscal 2025.

- Americas: Up 3% for the full year.

- EMEA: Down 2%.

- APAC: Down 1%.

Vans: Americas DTC Returns to Growth, but Full Recovery Remains in Progress

Vans declined 5% in constant currency in Q4 and posted an 11% full-year decline.

Revenue for Vans is expected to decline mid-single digits in fiscal 2027.

Still, executives cited pockets of progress. Vans returned to growth in Americas DTC for the first time in almost four years, a milestone Darrell highlighted as evidence that the brand’s repositioning is beginning to connect with consumers.

The Authentic silhouette was the clearest bright spot. The shoe delivered 80% revenue growth in Q4 versus the prior year. Slip-ons also returned to growth during the quarter.

VF attributed some of the improvement to the brand’s Off the Wall marketing campaign, which was anchored around the Authentic and generated improved search and engagement trends in key markets.

Vans’ new global “Off the Wall” global brand campaign. Photo courtesy of VF Corp.

New Vans Global Brand President Sun Choe has focused on product rationalization and speed to market. According to VF executives on the earnings conference call, the brand pulled forward products originally planned for Fall 2026 and delivered them in less than six months. The faster go-to-market process allowed the team to test silhouettes on a smaller scale, read consumer responses, and make sharper line adjustments.

Vans is currently shifting away from volume-driven assortments toward premium, target-market product drops. Product updates center on structural enhancements to shoe uppers and premium executions. To drive global demand, Vans has pivoted toward a social-first, culture-led marketing framework that utilizes high-tier collaborations, targeted retail energy drops, and broad-scale event activations.

Darrell said on the call that while Vans continues to manage inventory sell-in cautiously with wholesale accounts, DTC is serving as the blueprint for the turnaround.

“Our DTC is a good harbinger of what’s going to come, because the products that we have in our DTC are coming,” he said. “One by one, they’ll come into the wholesale network, online and offline.”

Vans Global President Sun Choe at NRF 2026. Photo by SESO.

The North Face: Footwear Investment Pays Off, U.S. Ski Partnership Announced

The North Face was the clearest growth engine in the portfolio. Q4 revenue totaled $935 million, up 7% in constant currency globally, with the Americas up 16%.

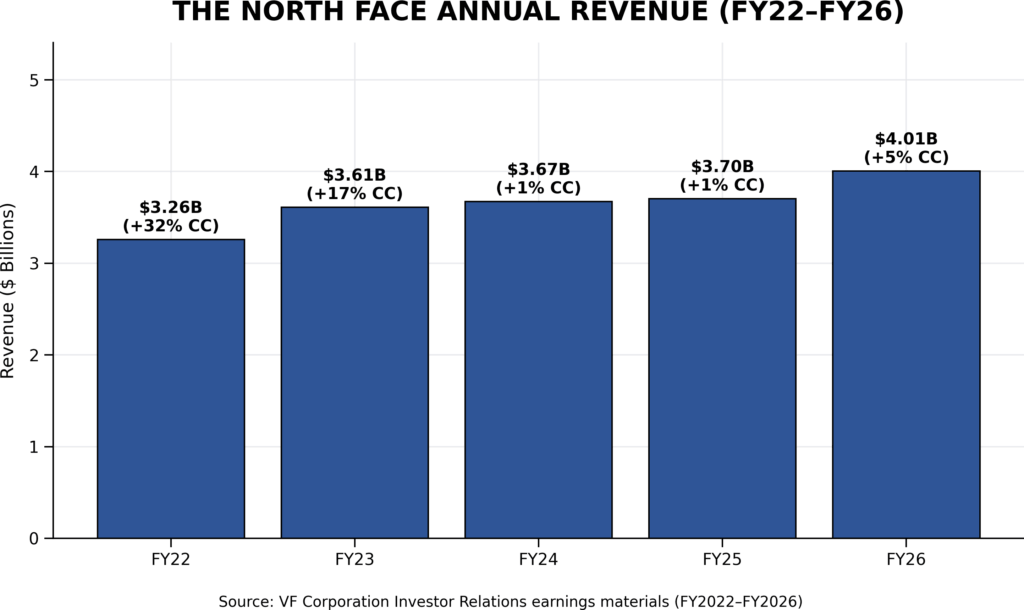

For the full year, North Face revenue totaled $4.01 billion, up 5% in constant currency.

Darrell pointed to broad-based category strength as the driver. Softshells and fleece were key apparel contributors in the quarter, while the brand’s footwear investment continued to deliver, with five consecutive quarters of double-digit growth.

New North Face Global Brand President Chris Goble. Photo courtesy of VF Corp.

To maintain premium brand positioning, The North Face has continued a targeted strategy of product elevation. Operational milestones highlighted in the earnings presentation include high-end lifestyle capsule introductions, such as the Casentino Wool collection, and premium expansions to core equipment lines like the Base Camp Leather Duffel. Brand executives said that there is a vast runway to double the size of The North Face over time via strategic category extensions, market share gains, and scaling higher-priced, premium interpretations of core garments.

The North Face also recently announced a new multi-year strategic partnership as the exclusive performance apparel sponsor for the U.S. Ski & Snowboard teams through at least 2034. Under the agreement, elite athletes will wear the brand across all global competitive circuits, including World Cup events and the Winter Olympic Games.

Darrell said that the company is taking measured steps to expand the brand’s long-term addressable market:

“There are so many ways we can grow this brand. Category growth, market share growth, new categories we can expand into, and finally, elevation to more premium versions of the products we already sell at higher price points,” he said.

The North Face’s recent revenue trends. Data verified by Shop Eat Surf Outdoor, visualized using AI.

Altra: Big Growth Ahead

Altra was the fastest-growing brand in the VF portfolio. Q4 revenue rose 45% in constant currency, driven by broad-based growth and new product launches. For the full year, Altra grew more than 30% and surpassed $270 million in revenue.

Darrell credited new launches and geographic expansion for the brand’s acceleration, calling the growth broad-based across all markets.

Executive Comments: VF Turnaround “Shows Up in the Results”

VF’s leadership team used the earnings call to say that the company’s transformation has moved from strategy to execution.

Chief Transformation Officer Abhishek Dalmia said the shift is visible in how the company operates day to day.

“What gives me energy is that transformation is no longer just a plan or a set of initiatives,” Dalmia said on the earnings call. “It shows up in the way we operate, the decisions we make, and the results we are delivering.”

Darrell pointed to margin expansion, leverage reduction, and top-line growth as the three pillars of VF’s recovery.

“Our results demonstrate that our strategy is working and that we’re well on track with VF’s transformation. I’m very confident in our ability to drive strong performance and shareholder value in the years ahead,” Darrell said in a statement.

Structural Changes Under Bracken Darrell

Darrell, who assumed leadership on July 17, 2023, inherited a company that was weighed down by debt and declining revenue. His turnaround template, “Project Reinvent,” has centered on cost discipline, operational optimization, and a focus on brand and product excellence.

According to VF Corp.’s financial disclosures, major transformations executed under his tenure include removing more than $225 million in structural SG&A expenses from the corporate run rate, rebalancing supply chain distribution logistics, and consolidating inventory networks.

To repair the parent company’s balance sheet, Darrell executed portfolio divestitures, selling streetwear brand Supreme for $1.5 billion in cash in 2024 and workwear brand Dickies for $600 million in cash in late 2025.

Money generated from these sales helped VF pay down more than half of its net debt (excluding lease liabilities) over the past three years. Total company net debt dropped from a peak of $5.8 billion down to $2.7 billion, dropping consolidated debt leverage from 5.1x to 2.0x (excluding lease liabilities) at the close of fiscal 2026, according to the company.

Bracken Darrell presents at VF Corp.’s Investor Day on Oct. 30, 2024. Photo courtesy of VF Corp.

VF Corp. Fiscal 2027 Outlook

VF provided the following guidance for fiscal year 2027, all figures in constant currency:

- Full-year revenue: Up 1% to 2% vs. fiscal 2026.

- Adjusted operating margin: Approximately 8%.

- Free cash flow: Flat to up vs. fiscal 2026’s $405 million.

- Year-end leverage ratio: 2.6x to 2.9x.

The company reiterated its medium-term target of a 10% operating margin exit run rate in fiscal 2028 and a leverage ratio of 2.5x or lower by fiscal 2028.