Key Takeaways:

- Nike widened its revenue decline guidance to low- to mid-single digits for the first two quarters of fiscal 2027.

- Fourth quarter net income rose 407% to $1.1 billion, but the gain came almost entirely from a $986 million tariff recovery benefit.

- Sportswear and Jordan Streetwear remained the weak spots, while North America stayed the strongest region and Converse revenue fell 31% for the year.

Nike, Inc. reported fourth quarter and full year fiscal 2026 results Tuesday, posting flat full-year revenue and a fourth quarter net income jump that was almost entirely the product of a one-time tariff recovery.

Nike now expects revenue to decline in the low- to mid-single digits through the first two quarters of fiscal 2027, CFO Matt Friend said on the company’s earnings call Tuesday, citing a more cautious consumer and softer sell-through trends.

“The operating environment became more challenging as we progressed through the quarter,” Friend said Tuesday on Nike’s fourth quarter earnings call for fiscal 2026. “After a stronger start in March, especially in North America, by mid-April, we began to see a deceleration in retail sales trends. Our consumer is under pressure around the world, and we can particularly see it having a larger impact on Sportswear, which declined double digits in the quarter with a similar decline in retail sales.”

Nike CEO Elliott Hill struck a similar note in his prepared remarks, pointing to Nike Sportswear and Jordan Streetwear as the categories most exposed to that pressure.

“Overall, the results aren’t there yet,” Hill said. “We know we’re not living up to our full potential, particularly in Nike Sportswear and Jordan Streetwear, where sell-through remains challenged, impacting both current discounting and future order books. We’re operating in a more complex macro environment where we’re seeing added pressure on traffic and discretionary spending across our geographies.”

Friend attributed the wider guidance range to that softer sell-through combined with a tougher macro backdrop, and said the company is responding by tightening buys and reducing future sell-in.

“We now expect revenue to be down low- to mid-single digits, with Q2 having a sequential deceleration from Q1 due to some unique factors equating to a multipoint headwind, including higher digital promotions in the prior year in EMEA and timing of North America wholesale shipments,” Friend said.

Matt Powell, Senior Advisor at BCE Consulting, said the slowdown Nike flagged in April reflects a broader pullback across the industry, not a company-specific issue.

“This is not just a Nike issue,” Powell said. “The slowdown is happening across the industry, driven by high gas prices, inflation fears and, frankly, a lack of great product. No brand or retailer is immune.”

Powell added that weakness in Nike Sportswear highlights the discretionary nature of the category and the importance of newness.

“Sportswear is totally a discretionary purchase, driven by a fashion consumer looking for newness and excitement,” he said. “The lack of fresh product at scale is an industry-wide issue.”

Nike Fourth Quarter Financials

• Revenue was $11.0 billion, down 1% on a reported basis and down 4% on a currency-neutral basis.

• Net income was $1.1 billion, up 407%, and diluted EPS was $0.72, including a $0.52 per share benefit related to the expected recovery of IEEPA tariffs.

• Excluding the tariff benefit, EPS was $0.20.

• Gross margin rose 890 basis points to 49.2%, including a $986 million benefit from the expected IEEPA tariff recovery. Excluding that benefit, gross margin was 40.2%, down 10 basis points from a year ago.

• Wholesale revenue grew 4% on a reported basis and 1% on a currency-neutral basis.

• Nike Direct revenue fell 7% on a reported basis and 9% on a currency-neutral basis, with Nike Digital down 12% and Nike owned stores down 7%.

• North America revenue grew 3%. EMEA revenue fell 1% on a reported basis and 6% on a currency-neutral basis. Greater China revenue fell 12% on a reported basis and 17% on a currency-neutral basis.

Nike Full-Year Financials

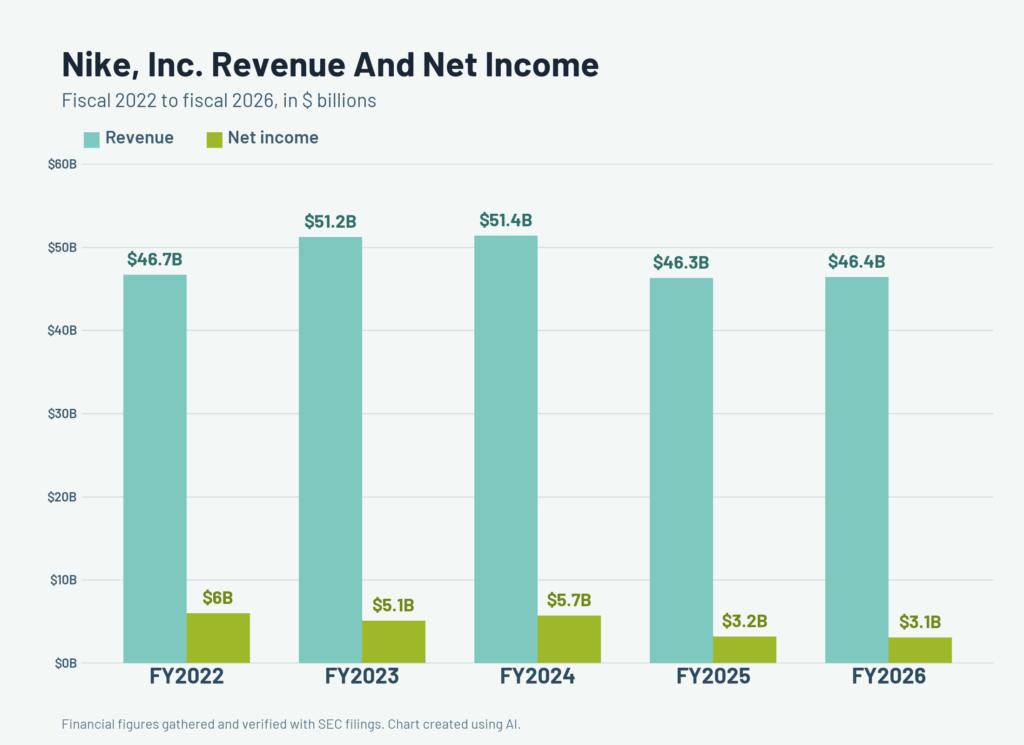

• Revenue was $46.4 billion, flat on a reported basis and down 2% on a currency-neutral basis.

• Net income was $3.1 billion, down 3%, and diluted EPS was $2.10, or $1.58 excluding the tariff benefit.

• Gross margin was 42.9%, up 20 basis points, or 40.8% excluding the tariff benefit.

• Wholesale revenue grew 6% on a reported basis and 4% on a currency-neutral basis, led by double-digit growth in North America.

• Nike Direct revenue fell 6% on a reported basis and 8% on a currency-neutral basis to $17.7 billion, with Nike Digital down 12% and Nike owned stores down 4%.

• Nike Running posted its fifth straight quarter of double-digit growth, adding roughly $1 billion in revenue over that stretch and gaining five points of running market share in statement footwear across North America and Western Europe.

Nike North America and the Consumer

North America remained Nike’s strongest market, with fourth quarter revenue up 3% and EBIT up 91% on a reported basis. Hill was bullish on the region’s trajectory. “They continue to lead the comeback,” Hill said, crediting the team’s focus on sport and its wholesale relationships.

Asked later in the call whether North America wholesale might decline in any quarter of fiscal 2027, Hill added, “I remain very bullish on North America and their ability to continue to have sustainable growth moving forward.”

Friend cautioned against reading too much into the headline wholesale number, though.

“When you look at Q4 and you look at the North America wholesale growth reported up 10%, I just want to make the point that we didn’t sell-in up 10%,” Friend said. “There was a meaningful amount of that revenue growth that was associated with lower returns or sales-related reserves and returns, lower discounts and lower cancellations. It’s a healthier business in North America that contributed to that growth in Q4.”

That healthier marketplace showed up in Nike’s results with Foot Locker.

“Our revenue growth and retail sales comp with Foot Locker was positive for the first time in four years, and we continue to be encouraged about the path ahead,” Friend said. Hill added that North America’s approach, centered on sport and a more disciplined wholesale relationship, is becoming “the model for the rest of the (geographies) to follow.”

Still, both executives acknowledged the region cooled as the quarter went on.

Nike Direct-to-Consumer

Nike Direct remained the softest part of the business. Fourth quarter direct revenue fell 7% on a reported basis and 9% on a currency-neutral basis, with Nike Digital down 12% and Nike owned stores down 7%.

For the full year, direct revenue was $17.7 billion, down 6% on a reported basis and 8% on a currency-neutral basis, with digital down 12% and owned stores down 4%.

Executives framed part of the decline as deliberate. Friend said Nike’s off-price digital sales in EMEA were down 50% from a year ago after the company pulled back sharply on promotions there.

“It’s the right decision,” Friend said. “It’s strategically what Elliot highlighted as he came in, that we need to reposition digital to be a premium business.”

Powell drew a distinction between Nike’s two core lifestyle engines, arguing that the challenges in Jordan may be more structural.

“Jordan was a $7 billion brand built on scarcity,” Powell said. “That model was broken during the previous Nike regime and may not be fixable.”

He added that the brand is likely evolving into a more everyday brand rather than one built on Saturday sell-outs.

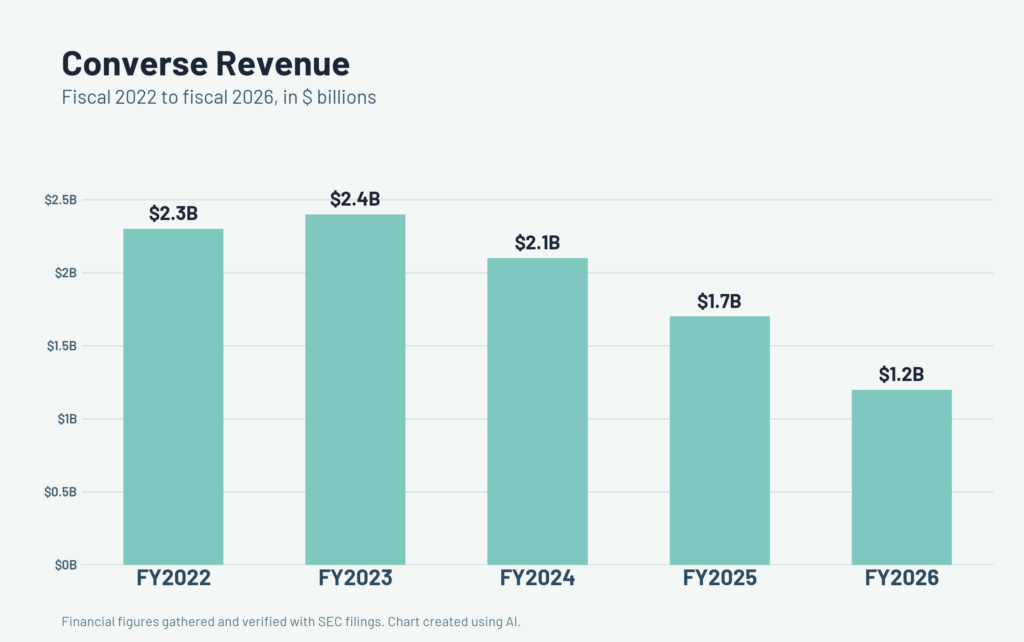

Converse Revenue Down 31% for the Year

Fourth quarter revenue fell 32% on a reported basis to $244 million, and full-year revenue was down 31% to $1.2 billion.

Hill said the brand narrowed its focus during the quarter. “Converse sharpened its strategy this quarter,” Hill said. “It’s getting clearer on the role it plays within Nike, Inc. and where it will grow, especially with the Chuck Taylor and Jack Purcell franchises.”

As part of that shift, Nike announced that NBA guard Shai Gilgeous-Alexander has joined Nike Basketball, a move Hill said “allows Converse to fully focus on serving creators through its lifestyle business.”

Nike Outlook

Beyond the top-line guidance cut, Friend said gross margin expansion is now expected to begin in the first quarter of fiscal 2027, earlier than the company had previously guided, with the improvement driven by cost actions taken in the supply chain over the past two quarters.

Nike’s tariff assumptions are built on a 10% incremental rate through the end of July, stepping up to 15% after that. The company will lay out its next phase of growth strategy at an Investor Day scheduled for November 16 and 17.

Powell said product innovation could help drive a recovery, particularly as Nike shifts toward a broader pipeline of launches.

“I don’t think we’ll see one blockbuster item, but rather dozens of items aimed at different sub-cohorts,” he said. “The fashion consumer is looking for freshness and newness, not products of scale.

“Nike is not back yet but is not far away,” Powell added.